Part V Perfecting an Article 9 Security Interest

Chapter 13 Overview Of Perfection By Filing

A. Generally

There are some important situations as to which filing a financing statement either is not permitted or is not advisable. However, filing is the action most commonly required to perfect a security interest and filing a financing statement is necessary to perfect an agricultural lien. See new 9-310(a).

The action of filing a financing statement may be conveniently separated into three inquiries. The first is what to file? The second is when to file whatever must be filed? The third is where to file whatever is required to be filed? As was true under former Article 9, the short answers to these questions under new Article 9 are that a secured party should file a document (or record) called a financing statement in the proper filing office and the filing should be done as soon as possible.

Understanding that filing as a mode of perfection is a two-sided coin is imperative. On the one side, filing is a step that perfects an interest in collateral against the claims of others to that collateral. On the other side, filing is the scheme by which third parties learn about the existence of interests in property that they are contemplating taking an interest in to secure a debt.

Stated differently, where to file and where to search are flip sides of the same coin. The governing rules may be understood (although not necessarily satisfactorily explained) as attempts to balance the burdens imposed upon filing parties and searching parties.

B. What to file

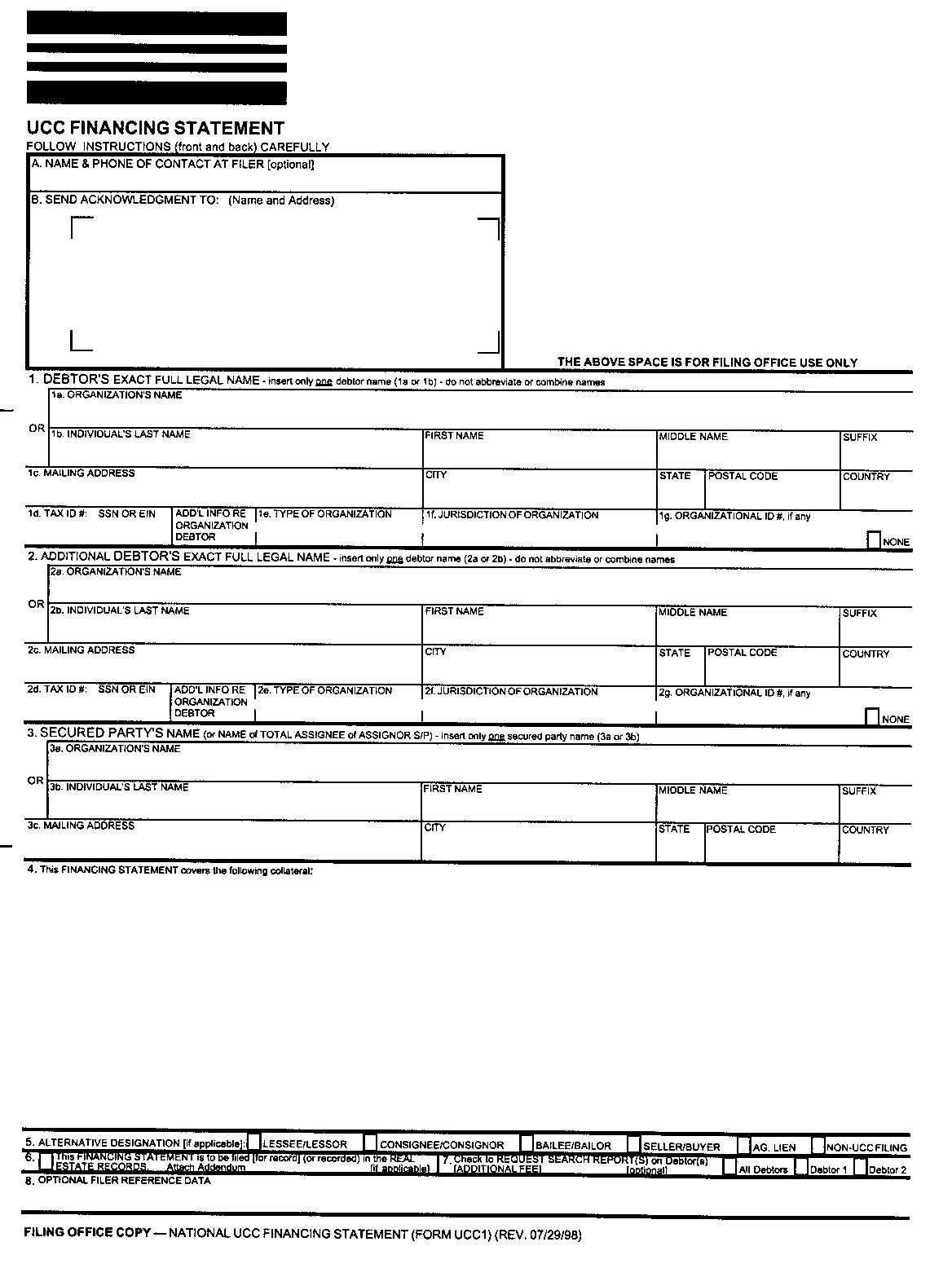

As was true under former Article 9 initial filings are made using a form called a "UCC 1." This form also may be used to continue and to amend initial filings. The contents of a UCC 1 are rather skimpy, at least by contrast to real estate recording instruments.

The reason is that Article 9 employs a "notice filing" scheme under which searchers are given only enough information to know that certain property of a particular debtor may be subject to a security interest. Under the notice-filing scheme it is incumbent on a searcher to make further inquiry to get the details of a possible security interest. See Official Comment 2 to new 9-502.

New Article 9 limits further the information that former Article 9 required to be included in a financing statement. For example, under former Article 9, section 9-402(1), a financing statement had to include the debtor’s address, a requirement that makes sense because, as is explained as third parties below, a third party must go through the debtor to obtain specifics about a security interests that the third party is put on notice of by financing statement. See subpart D (1) of Chapter 14 (The Nitty Gritty of Filing) infra. However, the debtor’s address is not included within the contents explicitly mandated by new sections 9-502, 9-503 or 9-504 for a financing statement to be sufficient under new Article 9.

Interestingly, as is explained in subpart C of Chapter 14 (The Nitty Gritty of Filing), a filing officer is required to reject a financing statement that does not include the debtor’s address and a financing statement that is rejected for this reason is not effective (although if the financing statement is accepted by the filing officer it very probably will be effective).

To facilitate electronic filing new Article 9 eliminates the need for the debtor's signature and refers at various places to "records" rather than financing statements. See new 9-502(a) and Official Comment 3 to new 9-502. The specifics of what must be contained in a financing statement are dealt with at length in Chapter 14 (The Nitty Gritty of Filing).

New section 9-521 contains a set of "safe harbor" forms that if properly completed must be accepted for filing by an office that accepts written records. There is a revised UCC 1 adapted to the requirements of new Article 9. To see what it looks like, click here.

Optimal protection against real estate parties of security interests in fixtures requires a "fixture filing." For a financing statement to be effective as a fixture filing the statement must indicate that it is to be filed in the real estate records, provide a description of the real estate to which the goods have or will be attached and, if the debtor does not have an interest of record, include the name of a record owner of the real estate. New 9-502(b).

Generally speaking, the description of the real estate is adequate if it reasonably identifies the real estate within the meaning of new section 9-108(a), as discussed in Chapter 8 (The Specifics of Enforceability -- A Security Agreement Authenticated by the Debtor or Its Equivalent). Optionally, a state may require that the description of the real estate be sufficient to satisfy the local law governing descriptions in real estate mortgages, including a legal description. New 9-502(b)(3) and Official Comment 5 to new 9-502.

The additional requirements for a fixture filing also apply to filings covering "as extracted collateral " (minerals and the like) and timber to be cut (but not timber that has already been cut). New 9-502(b). These additional requirements, and a provision under which a mortgage recording may be sufficient as to real estate-related collateral, are explored further in Chapter 14 (The Nitty Gritty of Filing).

Under former section 9-402(8), a financing statement that substantially complied with the requirements imposed by the UCC was effective. New section 9-506 is similar but it goes beyond the prior section to explicitly deal with the use of computers in filing offices and to address the "new debtor" problem discussed in Chapter 9 (The Specifics of Enforceability -- After-Acquired Property, Future Advances, Transferred Collateral and Proceeds and the New Debtor Problem).

The substantial compliance rule most often was invoked in disputes regarding the debtor's name and further discussion of the rule is best deferred to Chapter 14 (The Nitty Gritty of Filing) where the central role of the debtor's name in the operation of the filing system is explored.

As noted above, a major change from former Article 9 to new Article 9 is that the debtor's signature is not required. This change is designed to facilitate electronic ("paperless") filing. The elimination of the signature requirement does not mean that any and all filings are effective. New Article 9 spells out who is entitled to file a financing statement (or other record) and specifies that an initial filing must have been authorized by the debtor. See new 9-509(a).

New section 9-509(b) provides that by authenticating a security agreement (or becoming bound to it) a debtor (or new debtor) authorizes the filing of an initial financing statement and any amendment. The reach of new section 9-509(b) is worthy of comment.

It would seem that the scope of the authorization to file a financing statement is limited by the description of the collateral in the security agreement authenticated by the debtor. Thus, authentication of a security agreement containing a relatively specific description of the collateral should not authorize the filing of a financing statement that uses a much broader description (especially not a "super generic" description, as discussed below). The authorization scheme is considered at greater length in Chapter 14 (The Nitty Gritty of Filing).

New Article 9 provides for civil liability for unauthorized filings, spells out the effect of unauthorized filings and contains procedures for removing unauthorized filings. In so doing new Article 9 tracks laws in many states, including Arizona, strictly regulating recordings affecting real estate. See B & S (cited in Chapter 3), Ch. 13.

New Article 9 also adds a provision, new section 9-518, that allows a person who believes a filing is inaccurate or was wrongfully filed to file a correction statement. However, under new section 9-518(c) a correction statement does not affect the effectiveness of the filing with respect to which the correction statement was filed. See Official Comment 2 to new section 9-518. And, the drafters have taken the position that Article 9 cannot provide a satisfactory or complete solution to problems caused by misuse of the Article 9 filing system. See Official Comment 3 to new section 9-518.

Nonetheless, at least one state has enacted a non-uniform version of new section 9-518 that adds specific remedies for fraudulent and unauthorized filings. See Vernon’s Texas Code Annotated, § 9.5185. Remedies for unauthorized filings and other failures to comply with Article 9 are dealt with in Chapter 38 (Remedies for a Secured Parties Failure to Comply with Article 9).

The modifier "initial" is intended to distinguish first filings from amendments, continuation statements and an "initial financing statement in lieu of a continuation statement." See new 9-102(a)(39) (defining "financing statement") and new 9-102(a)(27) (defining "continuation" statement). The distinction is important in applying the transition rules of Part 7 of new Article 9.

As noted in Chapter 12 (Perfection Generally), and discussed further in the next subpart, in the end perfection is about priority and most priority disputes are decided according to some variation on the first-in-time rule. Consequently, the date and time that the financing statement was received for filing often can be critical. This information is provided by the filing officer. See new 9-523(a).

C. When to File

The when to file question is relatively easily answered. A financing statement should be filed as soon as possible meaning as soon as a client gets serious about extending secured credit to a debtor who is seeking such credit and the debtor has authorized the filing. The Article 9 filing scheme facilitates early filing. It does so insofar as it does not require that the agreement itself be recorded -- or even have been executed -- and by conditioning filing only on the debtor's willingness to authorize a filing. See new 9-502(d) and Official Comment 3 to new 9-502.

The reason for filing as soon as possible is that priority is largely a function of timing with the first-to-file often having priority. See Part VI. Early filing does not, however, assure priority over all other parties. The logic of the first-to-file priority scheme necessarily means that if another party is already on record when a creditor files then that other party is likely to have priority.

Because of the importance of timing in the Article 9 priority scheme there must be a rule for determining when a party is of record so as to establish that party's position for purposes of priority. Generally speaking, as was true under former section 9-403(1), a filing is effective when a financing statement is tendered together with any required fees. However, new Article 9 attempts to limit the wide discretion to accept or reject filings that filing officers had under former Article 9. See new 9-516 and 9-520(a). The specifics of the new Article 9 scheme as to when a filing is effective are complicated and best left for discussion in Chapter 14 (The Nitty Gritty of Filing).

A filing does not last forever. A financing statement is effective for five years at which time it lapses unless it has been properly continued. Consequently, there is another "when" to file question, namely, when it is necessary to make a further filing beyond the initial filing.

The need for another filing also can arise because of changes in circumstances that cause a financing statement to become misleading to searchers. These questions are dealt with at length in Chapters 23 (Continuing Perfection -- The Need to Reperfect (Or Refile) and 24 (Continuing Perfection -- Changes as to the Use of the Collateral or in the Location of the Collateral or the Debtor; Security Interests in Proceeds).

D. Where to File

Recall that there is a flip side to the where to file question, namely, where to search. The question of where to file (or where to search) actually involves two questions. The first is in which state a filing should be made. The second is where in the appropriate state the filing should be made.

1. Which State

As was discussed briefly in Chapter 6 (Choice of Law), the state in which to file a financing statement is the state whose law governs perfection and nonperfection (as distinguished from the effect of perfection or nonperfection).

Under former Article 9 the law of the state where the collateral was located (the "situs rule") was the state in which to file (or search) as to most tangible collateral, but filings as to accounts and general intangibles and mobile goods (goods that "normally" were used in more than one jurisdiction) had to be made in the state where the debtor was located (on the theory that intangibles had no situs and the situs of mobile goods was at best uncertain).

The choice of law rules provided in new Article 9 are intended to make answering the question in which state to file (and in which state to search) easier. As we saw in Chapter 6 (Choice of Law), the "general rule" is that the law of the state where the debtor is located governs perfection and non-perfection. Consequently, under new section 9-301(1) the state in which to file (and search) normally is the state where the debtor is located.

Under new Article 9, the law of the state where the collateral is located (the situs rule) governs perfection and nonperfection of possessory security interests, new section 9-301(2), and security interests in real estate-related collateral. See new 9-301(3) and 9-301(4). Under new section 9-302 a location of the collateral rule also governs as to the jurisdiction in which to file an agricultural lien. New section 9-301(3)(C), providing that the law of the state where the collateral is located governs the effect of perfection and nonperfection as to nonpossessory security interests (as distinguished from perfection and nonperfection) pertains to priority rather than perfection as such. See Official Comment 7 to new 9-301.

A location of the debtor choice of law rule means there must also be rules for determining where a debtor is located. These rules are found in new section 9-307. The place to begin is new section 9-307(b). The location rules of former section 9-103(3)(d) turned on whether a debtor was in business or not and did not distinguish individual from organizational debtors.

By contrast, new Article 9 divides debtors into individual debtors and organizational debtors. Under new section 9-307(b)(1) an individual debtor is located at the debtor's principal place of residence. Therefore, the state in which to file as to a consumer debtor or an individual business debtor is the state of the debtor's principal residence.

Under new section 9-307(b)(2), an organizational debtor is located at its place of business if the organization has only one place of business. New section 9-307(a) defines "place of business” as "a place where a debtor conducts its affairs." Under new section 9-307(b)(3), an organizational debtor that has more than one place of business is located at its chief executive office.

As was true under former Article 9, "chief executive office" is not defined. Official Comment 2 to new section 9-307 indicates that the chief executive office is "the place where the debtor manages the main part of its business operations or other affairs."

General partnerships and various unincorporated entities fall within the general definition of "organization" found in Article 1, section 1-201(b)(25) (formerly Article 1, section 1-201(28)). Under the location of the debtor rules for organizations, a general partnership debtor doing business in one state is located at its place of business, but if the partnership has more than one place of business it is located at its chief executive office. See Official Comment 2 to new 9-503.

Corporations are included within the general definition of an organization in Article 1, section 1-201(b)(25), but new Article 9 specially defines a "registered organization" in new section 9-102(a)(70). The gist of the definition is that if an organizational entity must be registered to exist then it is a registered organization. Under the definition, limited partnerships and corporations are registered organizations.

New section 9-307(e) provides that "a registered organization that is organized under the law of a State is located in that State." Consequently, a financing statement filed against a corporate debtor should be made in the state of incorporation. Likewise, the place to file as to a limited partnership is the state where the partnership is organized. Under new section 9-307(f), new Article 9 defers to federal law to decide where a debtor organized under federal law is located.

Under new section 9-307(c), new section 9-307(b) applies only where a debtor's residence, place of business, or chief executive office, as applicable, is located in a jurisdiction whose law generally requires information concerning the existence of a nonpossessory security interest to be made generally available in a filing or other registration system as a condition of priority of the security interest over a lien creditor. Where this condition of applicability of new section 9-307(b) is not met, the debtor is located in the District of Columbia.

According to Official Comment 3 to new section 9-307, as to a debtor who is a foreign national located in another country it is not enough that the law of that country includes a filing or registration system. It must also be the case that under this generally applicable foreign law filing is necessary to perfect, i.e., to get priority over a lien creditor. The law in many countries that have some form of filing or registration system, or which are moving to such systems, Mexico being a leading example, is likely to be less than clear on the matter of lien creditor priority. Consequently, a creditor may be well advised to file or record as required in the foreign country and also file in the District of Columbia.

It should be kept in mind that the new Article 9 rules that determine where a debtor is located, and more generally, the rules governing perfection and non-perfection of a security interest, are applicable only where the Uniform Commercial Code (UCC) governs a transaction. As explained in Chapter 6 (Choice of Law), in international transactions it is quite possible that the parties will choose the applicable law or the applicable law must be determined under choice of law rules and in either case it could happen that a law other than the UCC governs perfection and non-perfection (and other aspects of a transaction as well).

As noted earlier, security interests in real estate-related collateral often are subject to separate rules. Under new sections 9-301(3) and (4), a situs rule determines the law governing perfection and, hence, the place to file. Therefore, the state in which to file a "fixture filing" or to perfect a security interest in timber to be cut or minerals and other "as extracted " collateral is the state where the collateral is located. As also noted above, under new section 9-302 there also is a location of the collateral rule for agricultural liens.

Given that it sometimes can be difficult to choose the correct state in which to file, it would be natural for parties to attempt to make the choice in the security agreement. However, as noted in Chapter 6 (Choice of Law), for the most part, under the latest version of Article 1, section 1-301(c)(8) (formerly revised section 1-105(2)), parties may not choose the law governing perfection under Article 9.

2. Where in a State

As for where to file in the state whose law governs, the answer under former Article 9 depended on which of three alternatives to former section 9-401(1) had been adopted and further on whether the collateral involved required local or central filing. Local filing was done in the recorder's office of the county where the debtor was located. Local filing usually meant filing locally in the personal property records, but it also could mean filing in the real estate records. Central filing was filing in some central office, typically that of the Secretary of State.

New Article 9 works a significant change as to the rules governing the place to file within the state whose law governs. Under new section 9-501(a), central filing has become the general rule. The occasions for local filing are vastly more limited (although not any less important where required). Moreover, under new section 9-501(a)(1), local filing now means only filing in the real estate records in the office designated for the filing or recording of a mortgage.

Local filing is required to perfect security interests in "as extracted collateral," as defined in new section 9-102(a)(6), timber to be cut and security interests in fixtures IF the protection of a "fixture filing" is sought. See new 9-501(a)(1) and Chapter 20 (Perfection as to Fixtures and Other Real Estate-Related Collateral).

Under new section 9-501(a)(2), as to all other cases, including filings to perfect security interests in a fixture simply as goods (not a fixture filing) and timber that has already been cut, filing is central, meaning in a centrally-designated office, typically, the Office of the Secretary of State. See, e.g., ARS 47-9501(A)(2). New section 9-501(a)(2) also requires central filing as to agricultural liens even though, as noted above, under new section 9-302 the jurisdiction in which to file is that where the collateral is located.

Specialized filing rules apply under new section 9-501(b) to security interests in the property of a transmitting utility. In Arizona, for example, a filing in such cases is to be made in the Office of the Secretary of State. ARS 47-9501(B).

There was a rule in former Article 9 that provided a degree of forgiveness to a creditor who filed in the wrong place. That rule was found in former section 9-401(2). Proper application of the rule was the subject of considerable debate. There appears to be no comparable rule in new Article 9. Perhaps it is assumed that under the new filing scheme such a rule will be unnecessary.

The following problems explore the basics of perfection by filing under Article 9.

Problem 13.1 (interactive)

Sid Seller owns an appliance store in the City of Tucson, Pima County, Arizona. Betty Buyer resides in Tucson. Sid sells a new stereo system to Betty on credit. Betty buys the stereo for use in her home. The unpaid price of the stereo is secured by an interest in the stereo. For reasons that will be explored in Part VI, Sid prefers not to rely on automatic perfection.

In which state must Sid file to perfect the security interest in the stereo under new Article 9?

What language of new sections 9-301(1) and 9-307(b) supports your answer?

Where in the appropriate state should Sid file?

What language of new section 9-501(a)(2) supports your conclusion?

Problem 13.2 (interactive)

Lisa Lender is a New York bank. Lisa lends to Donald Debtor who is in the business of manufacturing automobile parts. Donald is a sole proprietorship doing business exclusively in the City of Tucson, Pima County, Arizona. Donald also resides in Tucson. To secure the loan, Lisa takes a security interest in Donald's inventory of automobile parts and equipment used in manufacturing the parts.

In which state must Lisa file to perfect its security interest in Donald's inventory and equipment under new Article 9?

Where in the appropriate state must Lisa file to perfect its security interest in Donald's inventory and equipment under new Article 9?

Problem 13.3 (interactive)

Suppose that the debtor in Problem 13.2 was an Arizona corporation, Donald’s, Inc., with its chief executive office located in Tucson, Arizona and that Donald’s is engaged in selling automobile parts in Arizona, California and New Mexico.

On the facts of Problem 13.2 changed to make the debtor an Arizona corporation selling automobile parts in Arizona, California and New Mexico with its chief executive office located in Tucson, Arizona, in which state must Lisa Lender file to perfect its security interest in Donald Inc.'s inventory under new Article 9?

What language of new section 9-307 supports your answer?

Problem 13.4 (interactive)

Suppose the facts of Problem 13.2 as changed to make the debtor an Arizona corporation selling automobile parts in Arizona, California and New Mexico with it chief executive office in Tucson, Arizona, were further changed in that Lisa Lender's security interest was in accounts generated by the sale of automobile parts (rather than the inventory itself).

Where must Lisa file under new Article 9 if the collateral is accounts and the debtor, Donald’s Inc., is an Arizona corporation with its chief executive office in Tucson, Arizona?

Problem 13.5 (interactive)

Suppose the facts are that the debtor is a general partnership, Donald and Donald, doing business in Arizona, California and New Mexico, Donald and Donald’s chief executive office is in San Diego, California, and Lisa Lender has a security interest in accounts generated by the sale of inventory in the three states.

Where would Lisa have to file under new Article 9 to perfect its security interest in the accounts?

Would the answer be the same if the collateral were inventory rather than accounts?

Would the answer change if Donald and Donald did business only in Arizona.

Could the parties specify the law governing perfection (the state in which to file) in their security agreement?”

Problem 13.6 (interactive)

Sid Seller operates a retail store in Phoenix, Arizona. Sid sells to Betty Buyer supplies to be used in Betty's farming operations conducted on Betty's farm in Marana (Pima County), Arizona. Betty is an individual. The supplies are sold on credit. The unpaid price of the supplies is secured by an interest in the supplies.

How should the supplies be classified?

As we have seen, the usual place for filing as to ordinary goods and intangibles is in the state where the debtor is located and in the Secretary of State's Office. Does your determination as to how the supplies should be classified require a different place of filing under new Article 9?

Note that Sid in such circumstances could have an agricultural lien as defined in new section 9-102(a)(5). Agricultural liens are within the scope of new Article 9 under new section 9-109(a)(2). See Chapter 4 (Scope of Article 9).

Where must Sid file to perfect an agricultural lien? Would your answer be different if Betty resided in California?

Problem 13.7 (interactive)

Second Bank, a New York bank, lends to Light It Up, Inc., a light bulb manufacturing business incorporated in Arizona and engaged in selling light bulbs exclusively in Arizona. To secure the loan Second Bank takes an interest in Light It Up's equipment, including a drill press in Light It Up's manufacturing plant in Tucson, Arizona. The drill press is attached to the floor of Light It Up's building in such a way as to give the holder of a real estate mortgage on the building an interest in the drill press (and, therefore, under new section 9-102(a)(41), the drill press is a fixture).

Will a filing in the Arizona Secretary of State's Office perfect the security interest in the equipment, including the drill press, under new Article 9?

As noted in the text, to gain whatever protection Article 9 provides against real estate parties Second Bank may wish to file a "fixture filing" (a specialized filing defined in new section 9-102(a)(40)). If Second Bank wishes to gain the additional protection of a fixture filing, where in Arizona should Second Bank file?

What section of new Article 9 governs the place to make a fixture filing within a state?

Would your answer to the question of where to file a fixture filing change if Light It Up's’s building were located in San Diego, California? If so, how?

Problem 13.8 (interactive)

Lisa Lender lends to Donald Debtor, an individual residing in Orange County, California, and takes a security interest in timber owned by Donald that is standing on land located on Mount Lemmon, in Pima County, Arizona. Lisa and Donald are aware that the timber will be cut and removed under a contract of conveyance.

In which state must Lisa file to perfect the security interest under new Article 9?

Where in Arizona must Lisa file?

Suppose the timber is a stand of virgin pine that there are no plans to remove? May Lisa perfect its security interest in the timber under Article 9?

What if the timber has already been cut when Lisa's security interest attaches. Where should Lisa file to perfect its security interest in the cut timber?

Problem 13.9 (interactive)

Donna Debtor creates a security interest in favor of Ready Lender. Donna authenticates a security agreement describing the collateral as "Debtor's inventory and accounts, existing and thereafter acquired."

Does Ready Lender have authority to file a financing statement indicating that the collateral is "Debtor's inventory, accounts and equipment, existing and after-acquired"? Before answering the question you may wish to consult new section 9-509(b).

As noted in the text, a creditor should file as soon as possible (for reasons of priority) and new section 9-502(d) indicates that a financing statement may be filed before a security agreement has been authenticated. When would a filing made before a security agreement has been authenticated be authorized?

Problem 13.10 (interactive)

Second Bank located in Tucson, Arizona is about to lend to Donald Debtor, an individual who resides and does solar electric installations in Rocky Point, in the State of Sonora, Mexico. To secure the loan, Donald has authenticated a security agreement giving Second Bank a security interest in Debtor's solar engineering equipment. The State of Sonora has recently implemented a registration system under which all nonpossessory security interests must be registered in a state registry in Hermasillo, Mexico, the capitol of the State of Sonora. Second Bank has registered its security interest in the registry in Hermasillo, Mexico.

Is Second Bank’s security interest perfected?

What action would you advise Second Bank to take?

Before answering these questions, you may wish to consult new section 9-307(c).

CASE COMMENTARY

In re Judith Baker, 430 F.3d 858 (7th Cir. 2005)

Planned Furniture Promotions, Inc. v. Benjamin S. Youngblood, Inc., 374 F. Supp. 2d 1227 (M.D. Ga. 2005)

Semmelman v. Mellor, 2006 WL 90094 (D. Minn. 2006)

Federal National Mortgage Association v. Okeke, 2006 WL 355241 (S.D. Tex. 2006)

In re Sabol, 337 B.R. 195 (Bkcy C.D. Ill. February 6, 2006)

First National Bank v. Lubbock Feeders, L.P., 183 S.W.3d 875 (Tex. App. 2006)

In re Millivision, Inc., 474 F.3d 4 (1st Cir. 2007)

Stockman Bank of Montana v. AGSCO, Inc., 727 N.W.2d 742 (N.D. 2007)

Alete, Inc. v. GEC Engineering, Inc., 726 N.W.2d 520 (Minn. App. 2007)

2009-02-01 update

{kind=link}